How our Economic Stories Shape the World: Long Now Video + Script

On Tuesday I spoke at the Interval in San Francisco for a Long Now Foundation talk. The Interval is my dream bar – it has a library which they dub a "manual for civilization," an office hidden behind a second-story bookcase, a spiral staircase, mechanical wonders, views of the Golden Gate Bridge, and so much more. The Long Now "is a nonprofit established in 01996 to foster long-term thinking. Our work encourages imagination at the timescale of civilization — the next and last 10,000 years — a timespan we call the long now." They have an incredible repository of talks, which I highly recommend!

I used this opportunity to interweave more of how I relate to and think about the world than my usual work. This talk is more authentically me. I hope you enjoy. The video is available here, and I've posted the script below with my slides interspersed.

Special thanks to my wonderful friends Mỹ Tâm H. Nguyễn and Olive Goh who came all the way from Seattle to join! 🥰 And to the incomparable Vicki Saunders, who came from Toronto to join me on stage for Q&A. Thanks to all my SF-based friends who also came out to join the conversation.

Watch the video here:

Embodied Economies: How our Economic Stories Shape the World

Part 1: A 4,000 year old story

Rounding a corner on the winding, forested road – dance partner to the island's perimeter – we came across a small public park. As the sun began to set – and the air infused with the crispness of fall’s yielding cycle – we felt beckoned, welcomed to divert our already meandering journey.

We followed winding paths into the lush Pacific NorthWest forest on a hilltop overlooking Puget Sound. Maple leaves larger than our heads formed a natural boardwalk, and the waves gently swooshed the ancient rhythm of water touching land. After some time exploring, we found a path that traced a small hill up and then down – widening into a most sacred sight: A perfectly constructed labyrinth – a swirling collection of stones draped in sunset’s riotous color.

I set foot on slick stone, the colors further deepened by afternoon rain. Each stone, pulled from surrounding beaches, had been selected and placed with the utmost care. Color variations – yellow, black, red, and white – formed bands streaking through the winding path.

Time seemed to stand still, elongate, and travel in reverse. It bent like origami. Time became tall as I walked atop centuries of tradition and ancient wisdom.

I only later learned that the late mosaic artist, Jeffrey Bale, had modeled the labyrinth after a 13th-century French cathedral while also including 12 rings to signify the seasonal and lunar cycles. The artist also incorporated four colors to invoke the Native American medicine wheel. The labyrinth was an homage to the rituals and spiritual paths across many centuries and traditions. Meditative walking – a human inheritance from all corners of the globe.

This experience connected me to a truth beyond my own body, beyond my lifespan, beyond my sense of a contained “self.” I found it difficult to sum up in words.

Language is necessarily derivative of our embodied interaction with the world. Before we have language, we have sensory experience, breath, and connectedness in the womb. Before we have language, we have the gift of a mother’s body, her food, and her energy.

Language becomes a mediated layer through which we try and relay our experiences in a multi-sensory world, a conduit. And then it becomes its own experience — its meta-structure of how we process and interpret the world.

Labyrinths like the one my husband and I found on Bainbridge Island near Seattle are an ancient archetype estimated to be around 4,000 years old, or more — not quite 10,000 years, but a fitting opening for this talk, I thought.

I didn’t know much about the history of labyrinths until preparing for this talk, though I’ve been drawn to them throughout my life and my spiritual practice.

One of the earliest known references to labyrinths is the myth of the Minotaur and the Labyrinth in Greek mythology, which dates back hundreds of years BC. In this myth, a half man, half bull – the minotaur – is imprisoned by King Minos and banished to wander a labyrinth until he is killed by Theseus, who finds his way back out of the labyrinth using a ball of thread given to him by Princess Ariadne.

This story inspired ancient Cretan coins.

And the form of the labyrinth has been incarnated all across the world as design elements in Roman mosaic floors, cathedral designs in the medieval Christian period:

in Italian and English gardens, and today as spaces for quiet reflection for all who enter.

In her transcendent Long Now talk "Saving Time: Discovering a Life Beyond the Clock", Jenny Odell shared that “The most important technology we’ve ever had is the story, but stories only work through the telling.” This story cascaded through 4000 years of human-embodied living and practice to find its way to me in Seattle, and to find its way to you - here tonight.

Labyrinths are a collective human story across cultures, time periods, and locations that have become physically embodied in places worldwide. Of course, there are many examples of this: A story, a ritual, made physically manifest.

Part 2: Stories and our Economic Storytelling

Our world is built on stories, paradigms, ways of understanding the world, and our role in it.

Neil Gaiman gave a talk here a number of years ago entitled "How Stories Last" in which he said that trees live 5000 years, animals live 300 years, and stories last much longer than that. Our oldest human stories have been passed from generation to generation and outlast any living creature, making them – in a sense – alive.

To me, nowhere is this more evident than in the stories we tell ourselves about the economy.

What is the economy? Actually quite a difficult question. One thing for certain, though, is that the economy is not a neutral thing. The language we use to describe it could lead us to believe that it’s a machine, one we can kick start with the right amount of stimulus money from nation-states or central banks. Or that it exists in the S&P 500, the global commodities market, or the amount of money circulating in the economy (M1, M2, M3 measurements of money supply, etc.).

But no – the economy is an emergent phenomenon largely based on adopted stories and the values they contain. And how these values become formalized through technology, law, and regulation.

One place where the values of an economic era manifest themselves is in the skyline of our cities. Take London – for example – where I lived for few years:

The skyline of London used to be dominated by religious buildings because the church represented one of the most powerful economic institutions of the time.

Later, as the role of the state grew as provisioner of public services and security, buildings like the Elizabeth Tower/Big Ben and large judicial and legislative buildings emerged with grandeur.

And now of course the skyline of London is dominated by banks, financial institutions, and luxury condos – which is also the case with many large cities globally today.

These stories, these paradigms, and notions of who we are as a species, quite literally scaffold the world around us. They embody and serve as the great monuments to our economic paradigms and cultural meta-memes of different eras.

These stories become embodied in the physical substrate of our world — they become institutionalized: through technologies, administrative processes and bureaucracy, case law, regulatory and policy documents and approaches. They ossify through feedback loops inherent to our systems.

Power centers or institutions – like the church, or the state, or financial markets – can orient the entire legal and financial apparatus around their entrenchment. They impose their values through encoding the law around their own protection.

As Katharina Pistor points out in her incredible book The Code of Capital: How the Law Creates Wealth and Inequality what we call “capital” is coded from a few legal modules that have long existed: contract law, property rights, collateral law, trust, corporate and bankruptcy law.

And two predominant legal systems – English common law and New York State laws – dominate global capital laws. London and New York house all of the top 100 law firms, as well as many of the largest global financial institutions.

She says: “This is where most capital is coded today, especially financial capital, the intangible capital that exists only in law. The historical precedent for global rule by one or several powers is empire. Law’s empire has less need for troops; it relies instead on the normative authority of the law, and its most powerful battle cry is “but it is legal.”

What is normative authority in law? Some version of collective agreement about what is morally or socially acceptable. We first create social and moral judgments about how to ascribe value in the economy, and we codify it in law – we allocate the law around the protection of those judgments.

Stock market “value” is a measure of expectations of future performance. And what are expectations? They are collective agreements containing baseline assumptions about the future, and its projections.

They are stories.

A question: What values do we want to manifest themselves in the skylines of our great cities in the future?

Part 3 – The Myth of Objectivity / Neutrality

When we observe the physical and sociocultural changes that result from economic regime changes, we can see that these paradigms and shifts are not neutral – they create winners and losers. And they shape our collective, lived reality, which in turn shapes us in a reflexive loop.

However, one of the persistent myths and stickiest modern stories of the economics discipline – which has gravely affected policymaking – is a myth of neutrality. That economics is a mostly objective, mathematical discipline.

Economics has, for the last two hundred years or so, started with this paradigm:

Bounded, autonomous, rational man – disconnected from natural systems, complex systems of interconnection, and maximalist to his own desires.

Economics started with this one locus or unit of creation and built an entire discipline from that locus — and of course, it was from the perspective of highly educated and wealthy males, which were not in any way representative of the whole of human experience.

This foundation became the backdrop against which most modern economics rests its intellectual axioms, despite wanting to present as a purely mathematical discipline.

Every individual is seen as a rational, atomized actor, in complete control of their choices within a neutral market. There is very little (if any!) recognition in traditional economic theory about how cultural narratives of bodily hierarchies (racism, sexism, ableism, ageism) affect market participation. All bodies are treated the same. In economics, we come with no history. We come to the market with no heritage.

This was a very effective way of masking power dynamics.

Social theorists, poets, activists, and other wisdom keepers across time have investigated power — from Machiavelli, Hobbes, and Aristotle to James Baldwin, Hannah Arendt, Angela Davis, Audre Lorde, and bell hooks. And yet, traditional economics is largely silent on power. It has little to no epistemological framework for understanding how power influences markets and our experience of them – despite power differences between persons being one of the most salient embodied experiences of human life.

Economists, however, tended to view these as problems outside of their domain, despite the enormous influence of our bodies on our economic participation and experience. Economics was seen as computational, scientifically rigorous, and objective.

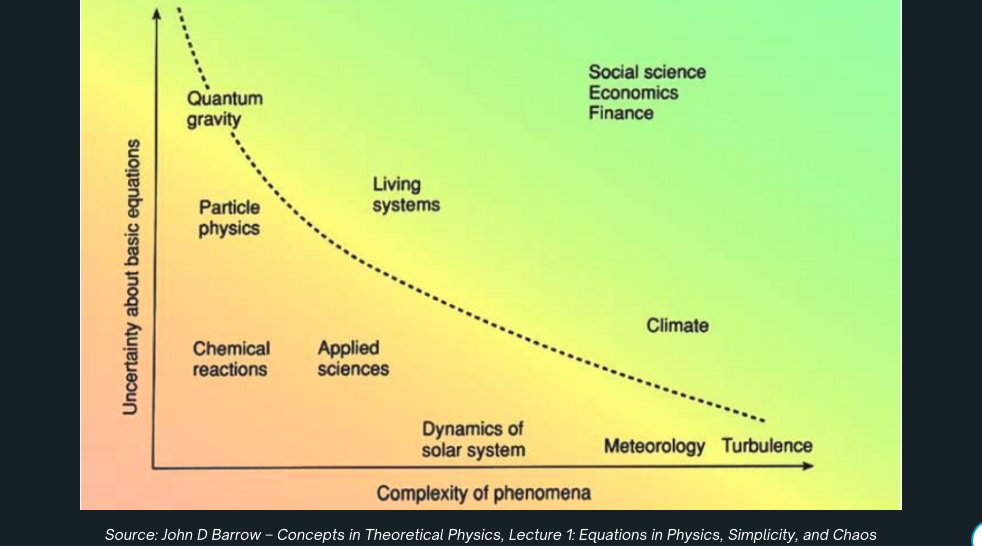

The below chart by British theoretical physicist, and mathematician John D Barrow shows a number of scientific fields. He has mapped them according to the complexity of the phenomenon on the x-axis, and the uncertainty about their basic equations on the y-axis.

So Turbulence is highly complex, but we know how to model it mathematically, whereas climate dynamics are more uncertain. Can anyone see where economics sits? High complexity, high uncertainty.

While other scientific disciplines like complexity science, dynamical systems science, and so forth disproved some of the foundational tenets and assumptions of neoclassical economics (like general equilibrium or individual self-interest aggregating into the highest social good), those with hegemonic power — in positions of influence in policy-making, the judiciary, and so on – maintain the status quo, though it is scientifically and visibly inaccurate.

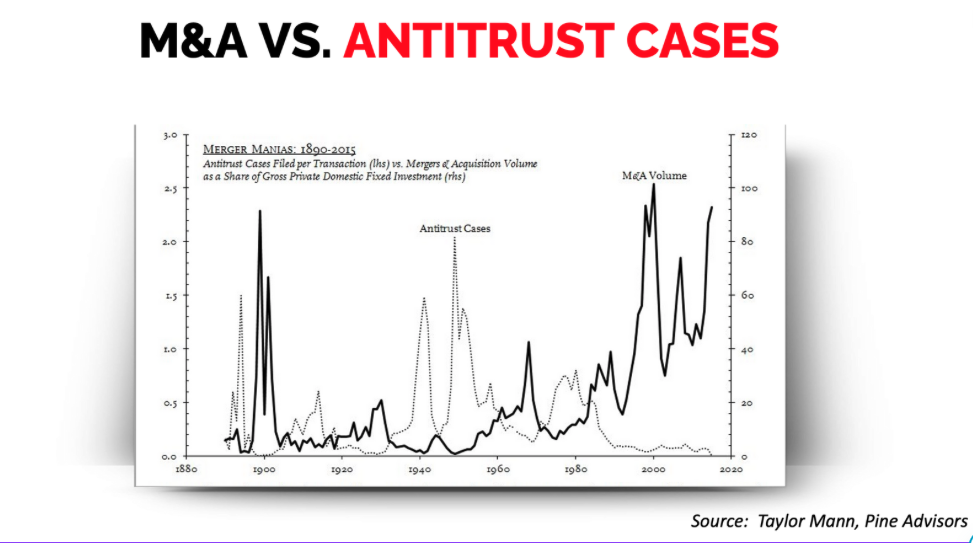

For example, in the domain where I work – competition policy and antitrust – economists have radically altered how the law is understood and enforced.

Antitrust – in the US – was originally focused squarely on the market power of dominant firms and using public power to resist de facto private regulatory regimes which undermined democracy. However, these concerns and questions about the role of the corporation in society were intentionally de-emphasized in the 1970s and 1980s with a strategy of intellectual capture and new normative interpretations of the law which emphasized ‘consumer welfare’ and ‘efficiency’ over other social goods.

Neoliberals also attempted to make competition policy more ‘neutral’ and ‘scientific’ by elevating the role of economists in adjudicating the law. Complex equations related to calculating market share, anti-competitive harms and benefits, and welfare were invented to – predominantly – serve the interests of merging parties. Firms claimed that efficiencies that would be gained through amassing market power (through M&A) would then be passed onto consumers in the form of lower prices.

Efficiency was seen as the highest social good – this was a value judgment, masquerading as mathematical rigor.

Of course efficiency and low prices are generally good things, and there are real tradeoffs to wrestle with regarding markets that benefit from economies of scale, network effects, and so on…but the undemocratic decision to make these things the normative goal of antitrust policy radically restructured the economy.

Competition policy’s narrow focus on consumer welfare (usually defined as low prices) over the last 40-50 years saw tech giants ascend to new heights with little to no scrutiny or challenges to mergers. A focus on lowering prices for consumers meant that new assetization strategies – such as monetizing a user’s attention while offering “free” products – went ungoverned by competition regulators. The Federal Trade Commission noted this problem in a September 2021 report showing that from 2010 to 2019 Alphabet, Amazon, Apple, Microsoft, and Facebook (now Meta) acquired 616 companies in a spree of acquisitions, and not a single one was blocked.

Non-price effects from concentrated markets like: threats to democracy or privacy, and effects on worker’s rights or the environment were mostly ignored. Mergers largely went unchallenged, leading to market concentration across many sectors of the economy which is well documented in the US, Canada, and Europe and increasingly so in other jurisdictions.

Perhaps most ironically, the promise of lower prices from efficiency gains largely failed to materialize. One study in the US by economist John Kwoka showed that when mergers led to six or fewer significant competitors in one industry, prices rose in 95% of cases after the merger. Because firms then have pricing power, which they can exercise against consumers, suppliers, or workers by way of lower wages.

We see this now continuing with private equity doing ‘serial acquisitions’ or rollups – where they purchase a number of small independent businesses and combine them for ‘efficiency gains’, but often for pricing power. They are doing this in everything from dental practices, to mobile home parks, to fitness gyms and psychedelic mushroom treatment centers.

This story – about efficiency gains, neutral economics, and so forth – has radically shaped economic allocation and led to higher inequality, among a number of now well-recognized social and economic problems like higher prices, lower worker’s wages, lower growth and innovation, fewer startups and so on.

Market fundamentalism – marked by a laissez-faire attitude towards public intervention in markets, created many of the problems we experience today.

I love this quote from a 1970s essay, “Tyranny of Structurelessness” by feminist author, Jo Freeman:

“To strive for a structureless group is as useful, and as deceptive, as to aim at an "objective" news story, "value-free" social science, or a "free" economy. A "laissez-faire" group is about as realistic as a "laissez-faire" society; the idea becomes a smokescreen for the strong or the lucky to establish unquestioned hegemony over others. This hegemony can be so easily established because the idea of "structurelessness" does not prevent the formation of informal structures, only formal ones. Similarly "laissez-faire" philosophy did not prevent the economically powerful from establishing control over wages, prices, and distribution of goods; it only prevented the government from doing so. Thus structurelessness becomes a way of masking power."

Liberalizing markets and granting them “freedom” was a philosophical – and practical – abdication of responsibility for the fundamental moral, ethical, and political questions about how we should organize terms of trade and public life.

Now of course, there are many economists who have been pointing out these fundamental flaws in economic reasoning for decades – many of them female and particularly women of color economists and academics, and of course activists and public policy advocates – but their work has been sidelined or deprioritized in the literature and in policymaking largely because it threatened established power structures.

My point is: All economics is political economics of one kind or another because it must start with a notion of human behavior, which is inextricably conjoined with moral and social dynamics and questions.

Part 4 – Profit Paradigms

There is an increasing disconnect between the logic of financial markets and planetary realities.

As we face down huge collective challenges like climate change, inequality, biodiversity loss, water usage, and so forth (meta-crisis, poly-crisis, etc.), many attempts have been made to deploy private finance to aid in the amelioration of these challenges. Estimates are in the trillions for climate change alone.

As a result, a proliferation of some formulation of this statement has occurred: people + planet + profit = (positive) impact

Impact investing, ESG, stakeholder capitalism, sustainable finance, etc. I’ve worked within these communities and researched many of these movements. However, I couldn’t get a question out of my mind: WTF is profit?

Profit seems like such an intuitive and self-evident concept that we rarely pause to reflect on it. A kind of primordial received wisdom, we assume a collective coherence about what it is. Total Revenue – Total Expenses = Profit.

But most accounting is not this simple nor straightforward.

And even if it were, how is profit derived? Who or what bears the cost of production of those profits (i.e. “externalities”), and what, then, is profit’s ultimate relationship (negative and positive) to “impact? and the collective good?

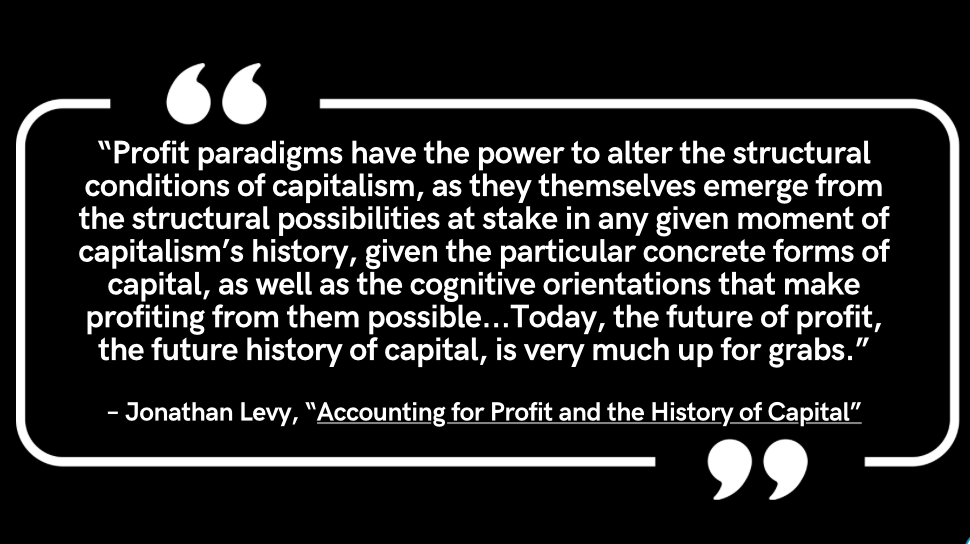

I found an excellent paper by Jonathan Levy, a professor at the University of Chicago who has written on this question: Accounting for Profit and the History of Capital. As Levy traces our evolving conceptions of profit over time, we come to understand that profit is not a constant or self-evident concept. In fact, our current way of accounting for profit is very young in the expanse of human commercial time. It is a new story.

Profit, as we conceptualize it today, did not exist before the mid-19th century.

Accounting in ancient societies was likely to take the form of credit and debit ledgers — as David Graeber says in his unparalleled book Debt: The First 5000 Years. “For most of human history—at least, the history of states and empires—most human beings have been told that they are debtors.” Indebtedness to someone else, or their indebtedness to you, was the primary method of account for most exchanges. Wealth, usually of kings, emperors, and nobles, was measured in long-range assets like land or political and militaristic power.

When the first global mega-corporations were formed (British East India Company in 1600 and Dutch East India Company in 1602), they were given their license to operate by royal charter and sought to expand the long-range assets of their respective empires. They did this by amassing (stealing) more land, tradeable goods (including, most horrifically, people), and political and militaristic power. These companies were granted a monopoly on global trade. The goal was not "profit" per se, but colonization, empire expansion, and wealth extraction.

Fast forward to pre-industrial (before 1850) enterprises in the US. This was the age of local, independent, and often family-owned businesses like stores, farms, and artisan shops. Before the mid-1800s, many firms did not track or report profits. We know this because, in the 1830s, the US Federal Government surveyed manufacturing firms to determine their rate of profit. The McLane Report, as it was called, was released in 1833. It showed that half of the survey respondents did not report a rate of profit (because they didn't measure it), they were just happy if they ended the year with a surplus.

Entering the industrial era, (1850-1920), profit came from lowering input costs (like labor). Profits tended to be reinvested in additional manufacturing plants and factories, railroad expansions, or steam engines as the Robber Barons built great industrial empires, controlling the infrastructure of commerce.As they grew in political power, arguments about the corporation's role in society reached a crescendo, and the first antitrust laws were passed (The Sherman Act in 1890 and the Clayton Act in 1914).

The mid-20th century saw the rise of the multinational corporation. Profit at this point becomes mostly an internal metric that helps make sense of diverse and dispersed corporate activities. Milton Friedman puts his ideas to paper and legitimizes the notion that greed (profit maximization) is a societal good.

Today’s profit regime I call: It’s better to sell Bitcoin than Teslas.

Our current profit regime (from the 1980s to the present day) has been irreversibly changed by the financialization of companies. Firms now use complex financing instruments, including derivatives, to adjust the assets and liabilities on their balance sheets. Corporate accountants adopted ‘mark to market’ or ‘fair value’ accounting methods during this period — the value of a company’s assets is based on what it could be exchanged for in the market right now. This, then, gets reflected in a company’s stock price.

Today, companies can earn 'profits' simply by rearranging the financial assets on their balance sheet instead of by providing high-quality goods and services. For example, in 2021, Tesla posted high profits for one quarter. But it didn’t earn these profits by selling cars. The company’s soaring profits were mostly from selling Bitcoin and carbon credits to other automakers to help them meet emissions mandates.

Today, around 90% of S&P 500 market ‘value’ is ‘intangible’ — as financialization has increased, the intangible value such as goodwill, intellectual property, patents, or trademark rights – created by collective imagination and coded into law, now dominates what we think of as economic health and vibrancy.

Profits of course can come from innovating and providing better products and services, but they too often come from erecting market moats — either by acting as a gatekeeper across a critical line of commerce and charging high tolls (like Apple taking 27-30% from app developers of every purchase in its App Store). Or, in the recent Department of Justice antitrust case against Google, we learned that in 2021, Google paid Apple $26.3 billion to be the default browser on Apple devices (to maintain its search monopoly). Which was 6.7% of Apple's global revenue!

These, and other dynamics, created a corporation that decoupled profit from productive investment. Companies are not interested in growing their businesses traditionally but are incentivized to find and exploit new collections of assets with which to pursue financial engineering and valuation expansions.

All this is to say that profit is not a straight-forward concept. How we understand and account for profit has major implications on the shape of markets. Jonathan Levy:

Part 5 – Stratigraphy

Many well-meaning attempts to restructure capitalism have yet to make tremendous progress on our many issues. There is no shortage of new economic thinking or new legal thinking — so why is the system so resistant?

One explanation is that the system is resistant to change because the legal and regulatory system is easy to game because the state largely protects capital through its legal enforcement mechanisms. Also that most innovations eventually have to graft onto the existing legal and financial infrastructure if they want to scale to any degree.

However, I would argue that in addition – the system is resilient to change because it is an emergent system that has been created out of our own fractured thought patterns.

In physicist David Bohm’s Thought as a System, he contends that there is a “systematic fault” in the whole of thought. And that "The pervasive tendency of thought to struggle against its own creations is the central dilemma of our time." – Bohm

The more I have dug into how decisions and debates are shaped, the more I’ve realized it's about terminology and language — which emanate from and co-shape thought.

Potawatomi – the language of the Potawatomi Tribe in the Great Lakes region – according to Robin Wall Kimmerer, has 70 percent verbs, as opposed to English, which has only 30 percent verbs, the rest largely nouns.

This difference connotes a kind of objectification in language, a conversion of aliveness and movement into static, fixed points.

New stories and new language are needed, or perhaps old stories — new to many of us stuck in Western ideological hegemony.

But luckily, the system is stories. The system is a series of moral judgments. The system is those values ossified through procedure, code, regulations, etc. These stories are changeable, these stories are rewritable, and are being re-written constantly.

There is a revival of industrial policy, economic textbooks are being re-written, a comeback of public utilities law, Canada dropped its efficiencies defense! Etc. Stories needs to be politically instantiated, and the tide is slowly turning.

Part of the challenge of 21st-century finance and economic policymaking will be how much we can hold economic reasoning back. In other words, to proscribe areas that the market should and will not touch. Things we refuse to assetize, monetize, commodify, or ascribe economic value to.

Attempts to apply market reasoning to everything from carbon markets to the newly created natural asset companies will not – on their own – solve our climate crisis. Because our profit paradigms bind them in ways that undermine their objectives and fall prey to the same power dynamics and fragmentation of thought that Bohm, Kimmerer, and others point out to us.

These and other economic puzzles can feel like mazes from which there is no way out...

But the labyrinth can offer us some lessons:

- This is both an individual and collective journey or quest which requires letting go of our certainties and desire for linear pathways

- The only way out is through

- The same form, can take on new meanings. Talismans like the labyrinth evolve over time, are built upon layers and layers of sedimentary thought and collective narrative. Perhaps the same talismans of economic storytelling — like profit or value – will evolve different meanings throughout time — more expansive, more liberatory, more equitable for all living beings.

The labyrinth teaches us that life is a continual flow that we participate in. And that any point in that flow is neither good nor bad -- it is simply part of the uncoiling journey leading us back to ourselves and to our shared sense of belonging here.

Many waves of humans – and our collective storytelling – have structured this world we call reality. Our buildings, our inventions, and our highest art — add to the layered stratigraphy of time, rising, standing, and falling in a cyclical pattern of human story.

When all of this – our buildings, structures, and physical embodiments of our cultural values are reduced to a layer of stratigraphy in the geological record – what do we want it to say about us?

May the long now inspire our moral imagination, to co-create a new story together.

Thank you.

Acknowledgements:

To a few of those who have shaped, informed, and challenged my thinking on the themes in this essay – to whom I owe deep gratitude: Katrine Kielos-Marçal, Michelle Meagher, My Tam Nguyen, Olive Goh, Vicki Saunders, Lisa Sachs, Audre Lorde, Donella Meadows, and many, many others.